Buffet Wrong on Capital Gains

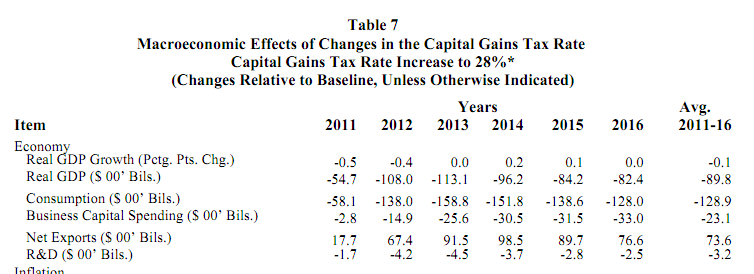

Warren Buffet is wrong on economic impact of higher capital gains rates. According to research by respected economist Dr. Allen Sinai, lower tax rates on capital gains had an important role in the post-2001 U.S. economic expansion. Sinai also notes the harsh economic consequences that the U.S. could face if rates are increased : Raising the top individual capital gains tax rate from the current 15% to 20%, 28% or 50%, reduces growth in real GDP, lowers employment and productivity and, ex-post, or after feedback, negatively affects the federal budget deficit. For example, at a 20% capital gains rate compared with the current 15%, real economic growth falls by an average of 0.05 percentage points per annum and jobs decline by an average of 231,000 a year. At a 28% rate, economic growth declines by 0.10 percentage points and the economy loses an average of 602,000 jobs yearly. When the capital gains tax rate is increased to 50%, real GDP growth declines by an average of 0.3 percentage points per year and there are an average 1,628,000 fewer jobs per annum. Buffet is also wrong when he says that higher capital gains rates won’t have a bearing on investment. In the…